THIS MATERIAL IS A MARKETING COMMUNICATION.

Eyeing China’s Solar Cells and Modules

The Evolution of China's Solar Cell and Module Industry

The manufacturing of solar cells is an intricate and fine business where the evolution of its equipment with technological improvement has been pivotal in product development. In contrast to a solar-grade wafer, cell manufacturing involves much more automation. The ingot is a piece of relatively pure material, typically metal, that is molded into a shape suitable for further processing. The ingot process in the manufacturing wafer needs to be controlled by a skilled technician due to the slight variation in the quality of polysilicon. Generally, the majority of solar cell work is able to be completed by machines as they are part of a standard manufacturing process. As a result, the advancement of equipment or production lines becomes an area of focus. Similar to that of solar-grade wafer producers, many cell equipment manufacturers come from semiconductor backgrounds. For example, Meyer Burger (Switzerland), Tempress Systems (Netherlands), Shenzhen S.C New Energy (China), and NAURA Technology (China) were semiconductor producers who later expanded into cell equipment manufacturing.

The technological improvement in the manufacturing process is directed at advancing the conversion rate. Currently, PERC is the second generation in solar cells. This generation has an improved conversion rate of about 22.5%1 under mass production based on traditional silicon solar cells. It has almost reached the potential limit of the silicon-based solar cell.

Therefore, the next generation of solar cells is working on heterostructures using other materials, as cost-cutting is the key answer for both cell and cell equipment makers. Module manufacturing is more of a replication business, using similar equipment, providing a homogenous product. In the past, equipment providers produced outputs that had been resembling production lines for other industries; therefore, it is a fairly mature business. It has been long known that China has been the leader in the business of replication for many years thanks to comparative advantage in cheap labor and land abundance.

The Drivers of the Industry Dynamics

There are four inputs in the production of solar cells: wafer, auxiliary materials (silver/aluminum), equipment, and labor. Citing the solar cell leader Tongwei's cost structure in 20192, wafer and auxiliary materials accounted for 84.1% of the total production cost, followed by equipment D&A and others totaling to 11.1% and labor at 4.7%. Similarly, the key inputs for a module are cell, labor, equipment, and energy, which make up 94.8%, 2.8%, and 1.5%, and 0.9%3 , respectively, according to Risen Energy's report. China leads the solar materials supply chain, which also benefits cell and module production from a cost perspective. There are a few cell and module capacities outside of China that focus on different technology routes. However, in the long-term, the expectation and trend will be for Chinese players to continually consolidate the market.

For the cell business, cash cost and sale price determine whether a business will suspend capacity in the short-term, as adequate liquidity is important for players to survive during a down cycle. However, similarly to the wafer business, besides cost, technology is another key factor that determines success or failure in the long-run. Downstream demand, equipment, and production process innovations drive solar cell developments accordingly. Businesses that are not well prepared for technological changes will ultimately fall behind the curveball and be driven out of the market. Once innovation reaches its potential, the lower the margin an industry has, the fewer new entrants there will be. It is relatively simple to decipher the consolidation landscape if we look at each player's capacity expansion plan. For module business, the consolidation may be driven by channel, especially to C business. Players that emphasize significance in building up their channels today are likely to succeed in the future.

Forward-Looking

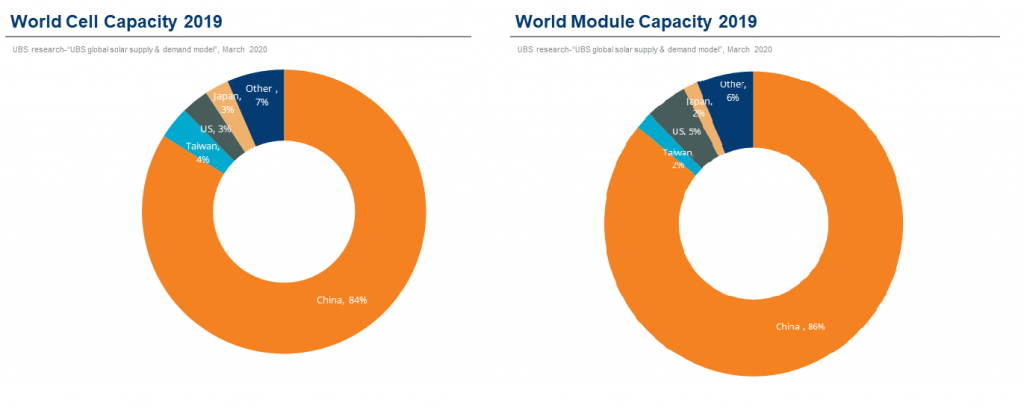

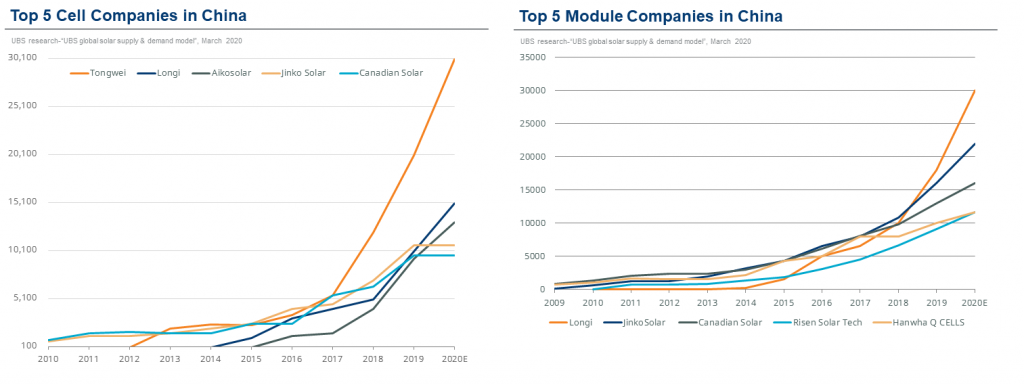

By the end of 20194, the top 5 Chinese solar cell producers comprised of a total market share of 33% in terms of capacity, while the top 5 module makers' total market share was 35%5 vs. polysilicon (56%) and wafer (70%). We can see from Exhibit 1 that both cells and modules are oversupplied. However, as technology is improving at exponential rates, the expectation is for costs to be lowered and efficiency to heighten. This will ultimately encourage end-demand and partially offset the oversupply. The current soft demand is likely to stop or delay small/new cell and module players' new capacity plans and benefit existing leaders, at least from a medium-term perspective.

In the long-term, the manufacturing business offers a relatively stable margin. If there is no special knowhow involved, then the cell and module margin will not be very high as it is with most of the manufacturing subsectors. We are likely to see module consolidation trends earlier than a cell. The reason behind this is that the module manufacturing process is already mature. As the current low margin environment continues, the industry is not attractive to new entrants. Existing leaders are able to build up their capacity and enjoy a large market share with low prices thanks to economies of scale. However, cell technology is on track to fast advancements. Capital could be a moat to stop small private enterprises, but the call for traditional energy SOEs is rising as they have decent access to funding and incentives to change, although, in our opinion, SOEs still have a long way to go. We cannot be assured that solar cell leaders today will be able to survive and consolidate the market in the future as there are still new entrants, and with new technological advancements, it will be a difficult task to predict the outlook of these businesses.

Disclaimer & Information for Investors

No distribution, solicitation or advice: This document is provided for information and illustrative purposes and is intended for your use only. It is not a solicitation, offer or recommendation to buy or sell any security or other financial instrument. The information contained in this document has been provided as a general market commentary only and does not constitute any form of regulated financial advice, legal, tax or other regulated service.

The views and information discussed or referred in this document are as of the date of publication. Certain of the statements contained in this document are statements of future expectations and other forward-looking statements. Views, opinions and estimates may change without notice and are based on a number of assumptions which may or may not eventuate or prove to be accurate. Actual results, performance or events may differ materially from those in such statements. In addition, the opinions expressed may differ from those of other Mirae Asset Global Investments’ investment professionals.

Investment involves risk: Past performance is not indicative of future performance. It cannot be guaranteed that the performance of the Fund will generate a return and there may be circumstances where no return is generated or the amount invested is lost. It may not be suitable for persons unfamiliar with the underlying securities or who are unwilling or unable to bear the risk of loss and ownership of such investment. Before making any investment decision, investors should read the Prospectus for details and the risk factors. Investors should ensure they fully understand the risks associated with the Fund and should also consider their own investment objective and risk tolerance level. Investors are advised to seek independent professional advice before making any investment.

Sources: Information and opinions presented in this document have been obtained or derived from sources which in the opinion of Mirae Asset Global Investments (“MAGI”) are reliable, but we make no representation as to their accuracy or completeness. We accept no liability for a loss arising from the use of this document.

Products, services and information may not be available in your jurisdiction and may be offered by affiliates, subsidiaries and/or distributors of MAGI as stipulated by local laws and regulations. Please consult with your professional adviser for further information on the availability of products and services within your jurisdiction. This document is issued by Mirae Asset Global Investments (HK) Limited and has not been reviewed by the Securities and Futures Commission.

Information for EU investors pursuant to Regulation (EU) 2019/1156: This document is a marketing communication and is intended for Professional Investors only. A Prospectus is available for the Mirae Asset Global Discovery Fund (the “Company”) a société d'investissement à capital variable (SICAV) domiciled in Luxembourg structured as an umbrella with a number of sub-funds. Key Investor Information Documents (“KI(I)Ds”) are available for each share class of each of the sub-funds of the Company.

The Company’s Prospectus and the KI(I)Ds can be obtained from www.am.miraeasset.eu/fund-literature . The Prospectus is available in English, French, German, and Danish, while the KI(I)Ds are available in one of the official languages of each of the EU Member States into which each sub-fund has been notified for marketing under the Directive 2009/65/EC (the “UCITS Directive”). Please refer to the Prospectus and the KI(I)D before making any final investment decisions.

A summary of investor rights is available in English from www.am.miraeasset.eu/investor-rights-summary/.

The sub-funds of the Company are currently notified for marketing into a number of EU Member States under the UCITS Directive. FundRock Management Company can terminate such notifications for any share class and/or sub-fund of the Company at any time using the process contained in Article 93a of the UCITS Directive.

Hong Kong: It is intended is for Hong Kong investors. Before making any investment decision to invest in the Fund, Investors should read the Fund’s Prospectus and the information for Hong Kong investors (of applicable) of the Fund for details and the risk factors. The individual and Mirae Asset Global Investments (Hong Kong) Limited may hold the individual securities mentioned. This document is issued by Mirae Asset Global Investments (HK) Limited and has not been reviewed by the Securities and Futures Commission.

Singapore: It is not intended for general public distribution. The investment is designed for Institutional investors and/or Accredited Investors as defined under the Securities and Futures Act of Singapore. This document is issued by Mirae Asset Global Investments (HK) Limited and has not been reviewed by the Monetary Authority of Singapore. Please consult with your professional adviser for further information on the availability of products and services within your jurisdiction.

Australia: The information contained in this document is provided by Mirae Asset Global Investments (HK) Limited (“MAGIHK”), which is exempted from the requirement to hold an Australian financial services license under the Corporations Act 2001 (Cth) (Corporations Act) pursuant to ASIC Class Order 03/1103 (Class Order) in respect of the financial services it provides to wholesale clients (as defined in the Corporations Act) in Australia. MAGIHK is regulated by the Securities and Futures Commission of Hong Kong under Hong Kong laws, which differ from Australian laws. Pursuant to the Class Order, this document and any information regarding MAGIHK and its products is strictly provided to and intended for Australian wholesale clients only. The contents of this document is prepared by Mirae Asset Global Investments (HK) Limited and has not been reviewed by the Australian Investments & Securities Commission.

Swiss investors: This document is intended for Professional Investors only. This is an advertising document. The Swiss Representative is 1741 Fund Solutions AG, Burggraben 16, CH-9000 St. Gallen. The Swiss Paying Agent is Tellco AG, Bahnhofstrasse 4, CH-6431 Schwyz. The Prospectus and the Supplements of the Funds, the KI(I)Ds, the Memorandum and Articles of Association as well as the annual and interim reports of the Company are available free of charge from the Swiss Representative.

UK investors: This document is intended for Professional Investors only. The Company is a Luxembourg registered UCITS, recognised in the UK under section 264 of the Financial Services and Markets Act 2000. Compensation from the UK Financial Services Compensation Scheme will not be available in respect of the Fund. The taxation position affecting UK investors is outlined in the Prospectus.

Copyright 2025. All rights reserved. No part of this document may be reproduced in any form, or referred to in any other publication, without express written permission of Mirae Asset Global Investments (Hong Kong) Limited.